SAP

Experiential Finance - banking in the age of the Millennials

Overview

SAP wants to help banks come up with new products and services to remain relevant in the future.

Team & Duration

Ashutosh Kole, Alyson Blume, Annabelle Ladao from General Assembly UXDi Winter 2015. Duration: 3 weeks

Tools & Methods

User Interviews, Secondary research, Affinity mapping, Concept model, Ideation, Competitive analysis, Storyboards,

Tools: Pencil & paper, Whiteboard

CHALLENGE

“I have an investment account but I do not invest actively”

The team was asked to formulate a strategy that banks could adopt in order to remain relevant in the future. The advent of mobile centered banking has caused a disconnect between end users and their bank advisors. As a result, a majority of the millennials, who grew up in the mobile age, end up passively saving their money in their banks instead of investing. They have a transactional relationship with their banks.

Lack of knowledge about investing (and money matters, in general) and lack of trust towards their banks, is causing the gap between Passive Savings and Active Financial Management.

Millennials want financial advice, strategies, and support but don’t see their banks as catalysts to financial well-being.

As a result, retail banks around the globe witnessed stagnation or decline in their ability to improve the customer experience and a corresponding increase in customers that are open to switching financial institutions. Retail banking customers today have more choices than ever before in terms of where, when, and how they bank.

Bringing the bank to the Millennials through the use of Artificial Intelligence, Virtual/Augmented Reality and Big Data; all through the common fabric of efficient social connections

The key experiential attributes which the financial institutions should follow in order to attract the millennials to have an engaged interaction with their financial institutions are Seamless, Instant, Personalized, Incentivized and Social. These are the Principles on which and financial activity should be based on.

The proposed financial model can be realized with the advances in Artificial Intelligence, Big Data, Virtual and Augmented reality. Our client, SAP, has expertise in these areas and they can help their banking clients realize the proposed model

“I think I would find it helpful if at least the institution that you are doing business with provided you with information for making smart investments, or said ‘hey, this might be something worth looking at.”

OUR APPROACH

The team started off by exploring the big ideas early on, taking the Double Diamond approach with an intention to go broad, as fast as we could, and then narrow down the focus to address the key pain point.

User Interviews with Millennials and Financial Experts

As part of our approach, we talked in detail with lots of Millennials in order to get some key insights into their financial habits and try to find some major roadblocks that prevent them from actively engaging with their financial activities. We especially focused on what key attributes they look for in a financial interaction. We also talked to banking experts to understand if and how banks are adjusting to their changing audience.

Distillation + Modeling findings

We had a lot of information to sift through after the interviews. We did affinity mapping to group the sentiments based on a particular financial activity.

We got some key insights based on the affinity maps. From that, we deduced some key requirements that we thought should be the basis of any financial model going forward.

The key experiential attributes which the financial institutions should follow in order to attract the millennials to their services are Seamless, Instant, Personalized, Incentivized and Social. These are the Principles on which and financial activity should be based on.

We mapped these attributes to the manner in which financial interactions take place as of today and concluded that current financial transactions do not provide all the above attributes mapped above. As a result, the millennials are not too keen on engaging in their own financial matters.

In order to bridge the gap between Passive and Active financial Management, financial institutions should create an experience based on the above principles to engage the Millennials. This can be realized using advances in technology. Advances in Artificial Intelligence, Virtual Reality, Augmented Reality and Big data, along with better ways of Social connections can facilitate this.

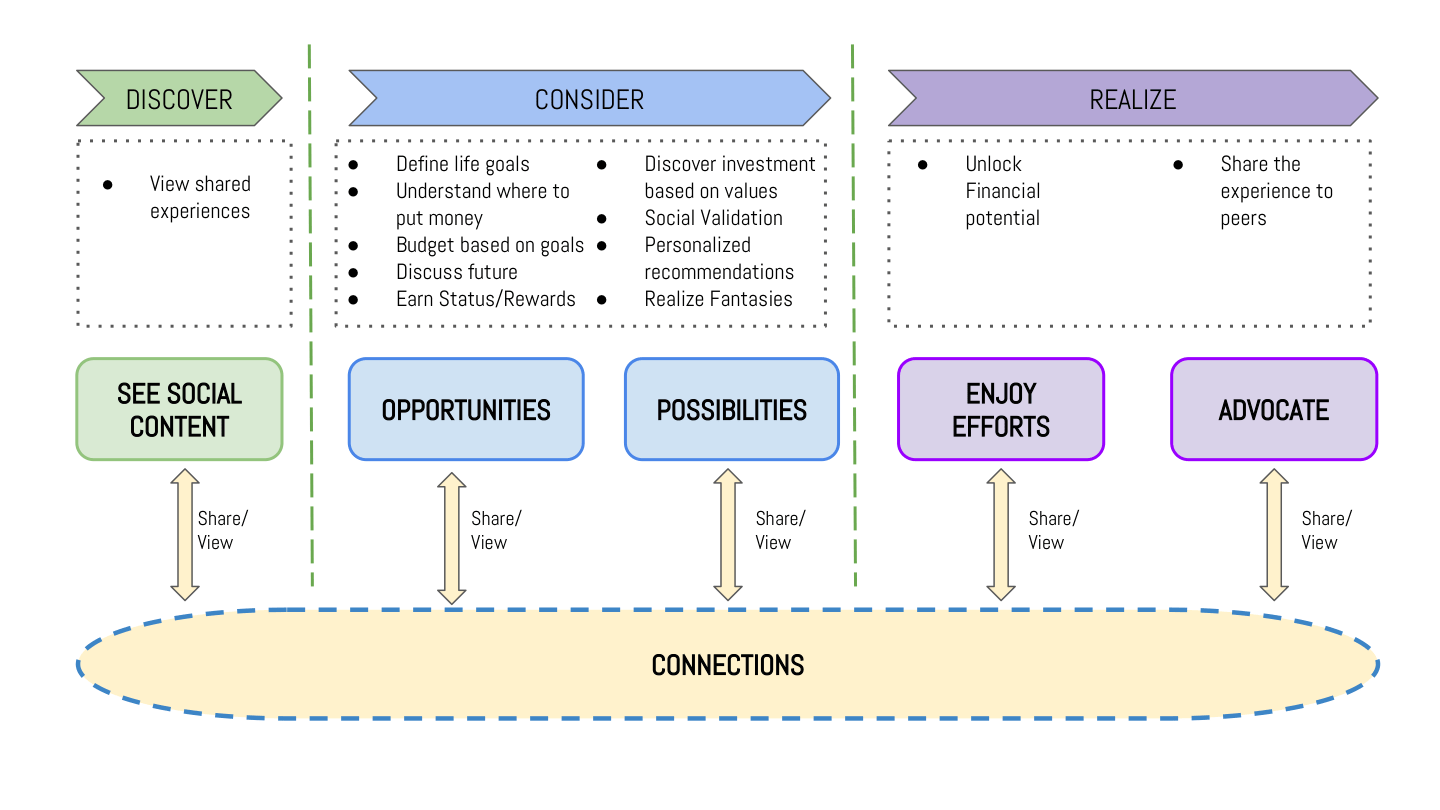

Experiential Finance Model

We mapped the progression of an end user’s financial journey towards financial realization and segmented that journey into classes. These classes are stages where financial entities have opportunities to provide service to engage the millennials.

DELIVERY MECHANISMS

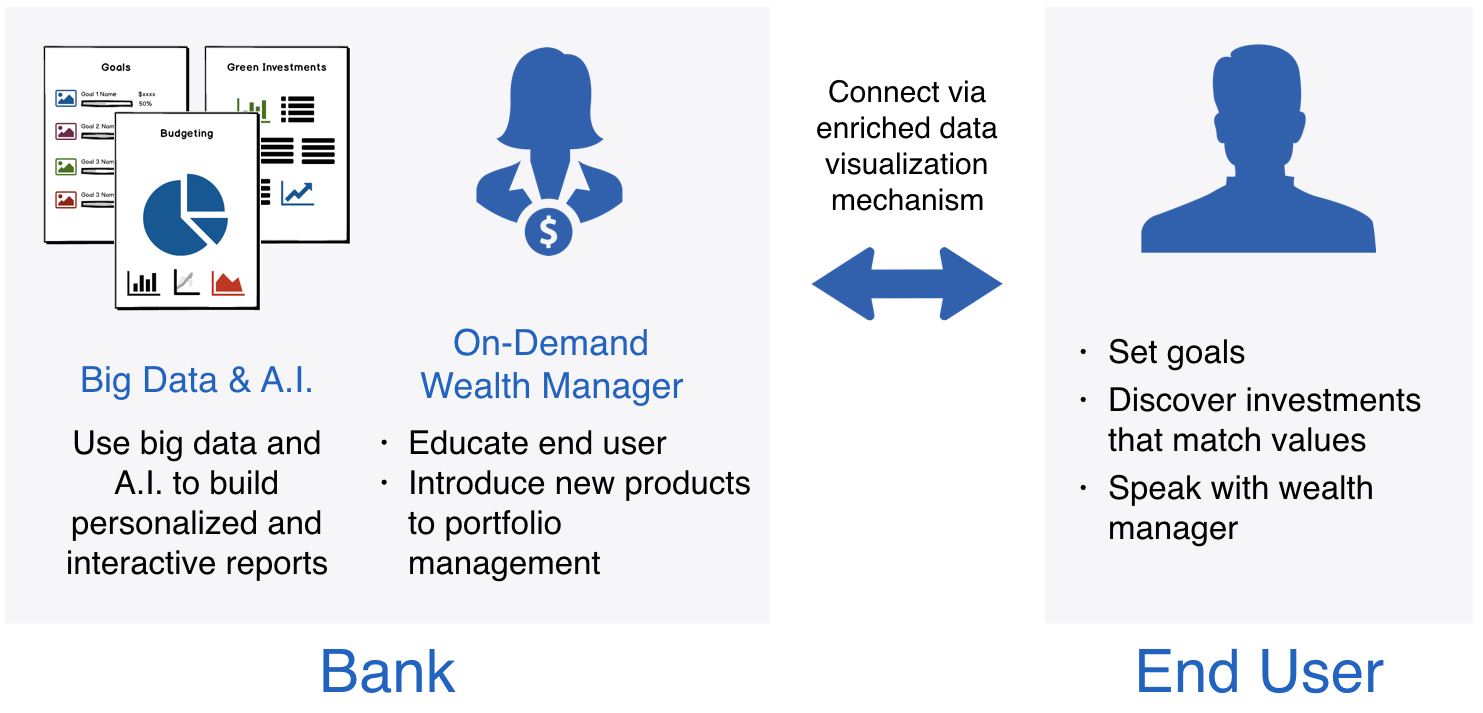

Data Visualization:

Presenting the data in an easy to digest, pictorial or graphic format is the most effective mode of communicating. Using A.I. and big data will allow all visuals to be highly personalized, dynamic and reflective of real-time information.

Using A.I., the bank can automatically tell when a user has excess money in their account, proactively send a message about their financial state and ask if they want help deciding how to manage their finances. Using smart home devices, the bank can project a hologram of a wealth manager to speak to users on-demand. Together, they can go through financial decisions, set goals and look at investments that meet the user's values in real time.

Immersive Storytelling:

Banks will be able to track spending against personal budget and investment goals in real-time. To help keep users motivated, they will be able to use Virtual Reality to immerse themselves in a fantasy world, where their saving and investing goals feel like reality and reward users for staying on track

Engaging interactive experiences that immerse the end user in a world where their short and long term goals already exist.

Connection:

“Social Media would make finance less intimidating”

Social connections form the basis of communicating your success story with your peers and help them to get into managing their finances to unleash their financial potential in return.

THE PROSPECT

There is a huge potential for this model to be self-sustaining. Social connection renders this model to have a feedback loop that engages other users into a journey towards financial fulfillment. The widespread use of Virtual and Augmented reality will be pivotal for the model’s success. Technology companies and Banks are already investing in the new visualization technologies along with Big data and AI.

More selected projects